With the changes in taxation of Dividend payments announced in the recent Summer Budget, we have produced a comprehensive guide for owners of SME’s to help them understand the potential impact on their income from April 2016 onwards. There are 3 easy to understand issues, the first of which gives a background to Dividends themselves.

BUDGET 2015 (CON)

Synopsis: A background to the reform of dividends announced in the Summer Budget.

This is the first of three bulletins on the subject of dividends and the reforms announced by the Chancellor in the Budget of 8 July. In this first Bulletin we look at the background to dividend taxation and how the new regime will operate from 2016/17. The next two Bulletins will look at the impact on investors and then on business owners. All three Bulletins are based on material published to date by HMRC/Treasury, which is sadly thin on detail. The necessary legislation is not due to emerge until Finance Bill 2016, so we are unlikely to learn much more until the draft Bill emerges, probably shortly after the Autumn Statement at the end of the year.

Dividend taxation is an awkward area for revenue authorities throughout the world. The major issue is whether and how to allow for the fact that the dividend payers – companies – generally pay corporation tax on their profits before making any distribution. In the USA, which has a much higher corporation tax rate than the UK, Uncle Sam does not bother and simply levies an additional 15% withholding tax on dividends.

In the UK, since 1973 we have had an ‘imputation’ system, which has attempted to give credit for some of the tax paid at the corporate level. Before Norman Lamont started messing around with this in 1993, UK dividends were treated as basic (standard) rate tax paid and came with a reclaimable tax credit equal to that basic/standard rate amount. So, for example, in 1992/93 a £75 net dividend would have come with an attaching tax credit of £25 which pension funds and other tax-exempt investors could reclaim. To make sure that tax was actually paid at the corporate level, there was advance corporation tax (ACT). This matched the dividend tax credit and had to be paid by the company even if it exceeded the corporation tax ultimately due.

In the 1993 Budget Norman Lamont took the first step towards breaking the system by reducing the tax credit to 20% (when basic rate was 25%) and creating a new dividend basic rate of 20%. This tweak had two benefits for the Exchequer: higher rate taxpayers paid more tax because of the smaller credit and, more significantly, the tax reclaim amount was reduced. ACT was cut to 20%, but the total corporation tax take did not change.

Wind forward to 1997 and Gordon Brown’s first Budget took Norman Lamont’s tweaking to the next level by reducing the tax credit and basic rate for dividends to 10%, with the ability to reclaim the credit withdrawn for pension funds immediately and from 1999/2000 for individuals (and PEPs/ISAs to come). For higher rate (40%) taxpayers dividends became taxable at 32.5% of the grossed up amount, i.e. an extra 22.5% was payable after allowance for the 10% tax credit. ACT continued at 20% for a couple of years, but was scrapped from April 1999. The demise of ACT effectively removed the last remnants of a direct link between the dividend tax credit and corporation tax paid.

It could be argued that in the July 2015 Budget, Mr Osborne brought the actions of his predecessors to a logical conclusion by scrapping the non-reclaimable 10% tax credit. In effect he has abandoned the imputation system and moved towards the US model. The Chancellor could have stopped it at that, adjusting tax rates for higher and additional tax payers to 25% and 30.56% of the dividend payable to produce the same tax income in 2016/17 as in 2015/16. However, instead he announced:

· A new dividend allowance from 2016/17 of £5,000 for all individual taxpayers; and

· New tax rates above the allowance of 7.5% for basic rate taxpayers, 32.5% for higher rate taxpayers and 38.1% for additional rate taxpayers – as the Chancellor said, a rise in all effective rates (based on dividend paid with no grossing up) of 7.5% (although actually 7.54% for additional rate taxpayers).

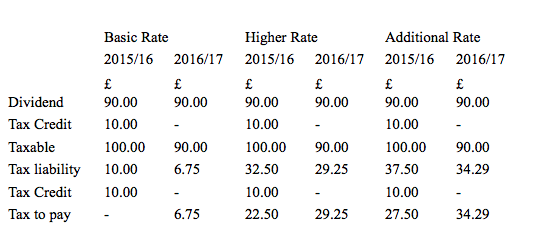

The net result is that 85% of taxpayers will be better off or at least no worse off, according to the Chancellor. For those above the new allowance a comparison of this and next tax year is shown below:

COMMENT

Chancellors of all hues prefer to increase the taxes that Joe Public does not understand and the dividend tax changes are a good example.

Why not talk to the professionals about properly managing your finances

Call us on 01273 457100 020 7871 5387 01403 333666

Or email us on info@opusgold.com

Or just take a look at how we help our clients www.opusgold.com